The Coronavirus Aid, Recovery, and Economic Support Act (CARES Act) was passed on March 23, 2020, under former president Donald Trump’s administration. This act was passed to mitigate the damage that the sudden and rapid emergence of the COVID-19 virus had on the economy in the United States—particularly local businesses—and the livelihoods of citizens.

Past Recessions and Government Action

The economic downturn caused by COVID-19 was not the first time that America has suffered a recession. For instance, in 1907, 73 financial institutions failed, primarily due to the bankruptcy of two small brokerage firms, which sparked distrust in companies and banks. However, this panic also convinced Americans that the government had a role to play in solving economic crises. In 1910, discussions about the formation of a central bank began, and by 1914, the Federal Reserve was created. Similarly, at the start of the Great Depression in 1929, the unemployment rate stood at 3.2% and peaked at 24.9% by 1933. To recover the economy, the Social Security Act of 1935 was passed, authorizing funds to be paid out to states (through the Social Security Administration), based on wages earned a few years before a beneficiary turned 65. Overall, the Great Depression changed the structure of the government and the general attitude towards the role of the government in solving economic crises.

Economic Provisions

Many provisions within the CARES Act directed financial support to businesses and individuals whose finances were directly impacted by COVID-19. For example, Section 2102 expanded unemployment compensation between January to December of 2020, granting 39 weeks of federal unemployment compensation to individuals who may have previously been ineligible under the laws of their state or territory. In addition, Section 1102 amended Section 7(a) of the Small Business Act by allowing the Small Business Administration to lend money to businesses that do not employ more than 500 people. This section required that such businesses use these loans solely to repay necessary business expenses, including compensation (i.e. wages and salaries, paid vacation time, health benefits, paid or unpaid leave, etc.) and utility costs. These measures provided money to both individuals and businesses to reduce the effects of the pandemic.

Housing Provisions

However, economic recessions and depressions not only impact employment prospects, but housing prospects as well. For example, not long after the pandemic began, tenants felt the impact of the contraction of the economy. Concerns over the spread of COVID-19 prompted private and governmental employers to either shut down or only partially open their workplaces, which left many employees, or residential tenants, without the stream of income that they had received before. Thus, the CARES Act also imposed a national foreclosure moratorium through Section 4022, and a national eviction moratorium through Section 4024, which ended in June 2021. Since the end of the foreclosure and eviction moratoriums, there has been a rising trend in eviction numbers. For example, since March 2020, Houston, Texas has seen 67,304 eviction filings by landlords, while Albuquerque, New Mexico has seen 9,339 evictions, and New York City 89,312. In response, states have supplemented provisions of the CARES Act with their own anti-eviction legislation. This provided tenants with additional time to make payments towards rent and business expenses. However, state moratoriums were also a temporary measure.

As a whole, the CARES Act provided temporary financial assistance to Americans. It gave money to individuals and businesses to support the recovery of lost wages and revenue and protected tenants via a federal eviction moratorium. However, as the measures within the CARES Act were only temporary, the future of American businesses, as well as American people’s tenancy and homeownership status, will depend largely on the state of the economy as it works to recover from the COVID-19 pandemic.

This past May, President Biden released his proposed budget plan for Fiscal Year 2022 (FY2022). The budget differs from budget plans in previous years in several notable ways. Itt proposes a temporary 15.5% increase in spending on non-emergency, non-defense appropriations—also known as non-defense discretionary (NDD)—which includes a wide array of services such as:

Education

Job training

Medical care for veterans (the largest program under NDD spending)

Scientific and medical research

Public health measures, particularly in the context of COVID-19

Treatment for substance abuse disorders

Housing and other assistance for families in need

National parks

Weather forecasting

The Coast Guard

International assistance

Air traffic control

Rural development

Upgrades to wastewater and drinking water treatment

This is a proposed increase in the NDD level excluding emergency funding distributed to address the pandemic, such as the American Rescue Plan Act enacted earlier this year. The FY2022 budget plan does not propose any further spending on emergency services.

This significant growth in NDD spending follows the recent expiration of the 2011 Budget Control Act, which capped the amounts spent on both NDD and Defense appropriations through FY2021. Due to the act’s stringent legal limits on the levels of both discretionary and non-discretionary spending, the only NDD category that saw an increase in appropriations through this decade was veteran’s medical care. Spending in this particular category was raised because of rising costs of healthcare and pre-existing shortcomings in the quality of healthcare available to veterans. More spending in veteran’s medical care led to tighter constraints for other NDD categories. The act caused 2021 NDD funding to be about 10% below what it was in 2011 once adjusted for inflation and population growth.

Overall, Biden’s new plan, free from the limit imposed by the Budget Control Act, focuses on using federal funds to begin addressing the racial and wealth inequalities currently present in the U.S. His administration plans to do this through the American Families Plan which substantially increases funding to education, child care, and housing assistance. The budget aims to foster equity in elementary and secondary school education, increase financial aid for college students, strengthen the public health system, meet healthcare obligations to tribal nations, address mental health and substance abuse, and make housing assistance and legal services for low-income people more accessible.

The budget also reflects significant reinvestment into critical institutions by increasing spending on federal research and development through the Center for Disease Control and Prevention and the Department of Health and Human Services. It also raises spending on environmental protection, reversing a decade of environmental funding cuts, particularly from President Trump’s presidency. It increased operating funds awarded to various agencies so that they could manage Social Security benefits, administer tax laws, and enforce laws that protect civil rights, labor standards, and workplace health and safety.

Effect on GDP and the Deficit

The Biden Administration estimates debt will grow to 117% of Gross Domestic Product (GDP) by the end of FY2031. In nominal dollars, this means the current debt of $22 trillion would reach $39 trillion. The increase in debt is due to the higher projected spending percentage of GDP relative to the revenue percentage. At present, the budget plan’s spending is 24.5% of GDP, while revenue is 19.3% of GDP. The percentages are higher than the 50-year averages of 20.6% of GDP for spending and 17.3% of GDP for revenue. Federal deficits would also rise to nearly $1.6 trillion over the next decade. However, Biden’s administration has announced plans to finance this deficit by gradually raising taxes for corporations and individuals with incomes over $400,000. In addition, the administration will continue to allow tax cuts for low to middle income earners that were originally put in place by the Trump administration.

Skeptics of the sustainability of Biden’s budget plan also cite his administration’s own low predictions for GDP growth despite tremendous investments in the nation. After accounting for inflation, the administration predicts the economy will grow about 2% a year—equal to the average rate of growth over the past 20 years. To this, Biden has said that current low interest rates and our unique position post-recession is the ideal time to invest in the nation. If his plan is approved, the government would be spending almost 25% of the U.S. output every year and would be collecting almost 20% of the total economy in tax revenue.

Committee for a Responsible Federal Budget and the Tax Foundation Analysis

The Committee for a Responsible Federal Budget is one such skeptic of the proposed budget plan. Their analysis concludes that the budget adds an unsustainable amount of debt over the next ten years while doing nothing to address high and rising debt in the long term. The Tax Foundation’s General Equilibrium Model echoes these concerns and further estimates that the budget plan will reduce GDP by 0.9%, and Gross National Product (GNP) by 1%, and also lead to 165,000 fewer jobs over time. Some of the primary contributors to these estimates are:

the increase in corporate income tax from 21% to 28%;

the 15% minimum corporate book income tax—which places a 15% minimum tax on the adjusted financial incomes of large corporations;

raising capital gains rates;

the increasing pass-through business income taxes, which increases taxes for businesses that are not subject to corporate income taxes.

The foundation estimates that the fall in GDP caused by the higher corporate taxes will offset any increase in GDP that may result from improved infrastructure and investment. The GNP, which is often used as a measure of American household incomes, is also expected to fall because of increased taxes on savers. However, Biden’s intent to only increase taxes for individuals earning over $400,000 in income and instead expand refundable tax credit programs for low- and middle-income earners indicates this will primarily impact high-income earners and savers. The taxes proposed in the budget support this estimate, and indicate the budget will lead to a 15.9% increase in the after-tax income of the bottom 20% of income earners. The model used by the foundation uses

A tax simulator to produce conventional revenue and distributional estimates,

A neoclassical production function to estimate capital stock and people’s responses to policy and how it impacts long-run output,

And a demand function to estimate people’s choices between labor and leisure as well as their choices between saving and consumption.

All together, the three components produce revenue estimates of tax policy and estimates how policy can impact GDP, wages, employment, and other indicators of economic performance. Similar to the Tax Foundation’s General Equilibrium model, the University of Pennsylvania’s Penn Wharton Budget Model looks more at the long-run effects up to 2050. This model predicts that the budget plan will result in a 7.3% decrease of public debt from what it is today. Overall, however, it estimates a 1.1% fall in GDP between now and 2050.

The Economic Policy Institute Analysis

The Economic Policy Institute (EPI) offers an alternative analysis, stating that Biden’s budget plan would have a host of positive effects if spending proposals not funded by increased taxes could be financed with debt. Their analysis indicates that the budget would result in an unemployment rate of 4.1% or lower over the 10 year period, reduced inequality through higher corporate taxes and better distribution of the benefits of economic growth, and a historically low public debt burden. This impact on equity is more difficult to measure and often is not easily translated into economic measures of success, which the EPI takes into consideration with their analysis. They further state that the Federal Reserve is not able to recover from recessions as quickly or efficiently as policymakers believe. A factor in this observation is the almost zero interest rate, which means it wouldn’t be sustainable to cut interest rates further, and subsequently indicating that fiscal policy can and should be a key contributor to economic recovery. Particularly given that this budget increases government spending and progressive taxes, it has the potential to be expansionary. The potential comes from its plan to make the budget deficit-increasing in the short term and deficit-decreasing in the long term. In addition, the budget entails a large growth in capital income taxes, which can reduce commuting time and increase quality of education when redistributed, ultimately making the economic growth more equitable. Finally, the EPI asserts that using the ratio of public debt to GDP is not an effective measure of fiscal burden because it is entirely retrospective and it divides a static stock measure—debt in a snapshot of time—by an income flow (meaning GDP) . It provides information about past budget deficits and does not take current policy into account. Using this retrospective measure as an indicator of budget success does not show the impact on equity.

Conclusion

Biden’s many goals coupled with the expiration of the 2011 Budget Control Act have resulted in unique deviances from past budget plans, including an increase in NDD spending relative to defense spending. His budget plan has also begun to center equity and reparations through education, public health, and housing assistance. However, the increase in funding required to further these goals have been called unsustainable by some and necessary by others.

Introduction to Free Trade and Comparative Advantage

Because of the economic principle of comparative advantage, free trade between countries is typically beneficial for all parties involved. One nation has a comparative advantage over another if it is able to carry out economic activity in a specific field at a lower opportunity cost in comparison to another country. For example, if country A can produce either 100 loaves of bread or 400 t-shirts in an hour, while country B can produce either 200 loaves of bread or 300 t-shirts in an hour, country B has a comparative advantage in the production of bread while country A has a comparative advantage in the production of t-shirts. In this scenario, and oftentimes in the real world, trade between country A and country B is mutually beneficial as country B can specialize in the production of bread, country A can specialize in the production of t-shirts, and they can each trade the good they produce for the other good that they do not.

Methods for Industry Protection

Sometimes free trade runs counter to a nation’s economic or political goals, like when an industry in one country is out-competed by an industry abroad. In these instances, the home country of the struggling industry may take a variety of actions to try to maintain their stake in the industry, such as:

Applying a tariff, a common trade restriction. Tariffs are taxes that are placed on certain imports on a product from another country, which typically increase the price of the good in markets in the importing country, encouraging consumers to buy products domestically rather than abroad.

Applying a quota, or placing a restriction on the quantity of goods that are imported. This limits the supply of the good and can increase the cost of making the product within the exporting country.

Providing home industries with subsidies, or monetary assistance. Rather than taking action against another country’s goods, the importing country can assist their industries by using government money to cover a portion of the cost of production. Subsidies can decrease the cost of supplies for the production of goods and thus allow the struggling industries to sell their goods at a lower price and still remain profitable.

Trade Agreements

Leaning too heavily on these protectionist measures can often escalate to countries using increasingly harsh trade restrictions, crippling foreign economies and decreasing economic efficiency. In order to avoid this outcome, countries will often establish trade agreements which outline rules of international trade that all members can agree upon and allow for fair competition. Established by the United Nations in 1947, the General Agreement on Tariffs and Trade (GATT) is an example of such an agreement. To resolve internal issues regarding dispute resolution, the GATT was replaced by a trade governing body known as the World Trade Organization (WTO) in 1995. The formal organization structure of the WTO and its amended rules were largely viewed as an improvement over the GATT. Currently the WTO consists of 164 member states, including the United States, meaning that it governs the vast majority of international trade.

The United States is also involved in numerous trade agreements with specific countries. The US establishes many Free Trade Agreements (FTAs) or Trade Promotion Agreements (TPAs) which allow for the free flow of trade between nations with minimal restrictions. In many of these agreements the US maintains a significant trade surplus, meaning that the US exports more to the other nation than it imports from them. Even in trade agreements where the US has a trade deficit, importing more than it exports, the US still gains valuable commodities and foreign investment in the economy. For example, in the US-South Korea FTA, the US has a trade deficit of $7.6 billion, but the volume of trade is valuable. The US exports $56.5 billion worth of goods while importing $77.5 billion. This trade agreement also creates about 358,000 jobs in the US economy. It is important to remember in these examples that trade is not a “zero-sum” game where the more you export the better. Imports can provide lower prices for consumers, greater variety, and an influx of materials necessary for the production of other goods.

Another type of trade agreement the US establishes with other countries are Trade and Investment Framework Agreements (TIFAs). These agreements outline the framework for future discussions on trade and investment between the two countries. These agreements allow for annual council meetings between the countries involved to negotiate on a wide range of trade issues without the agreement setting any explicit trade rules. The US also partakes in many Bilateral Investment Treaties (BITs) with countries where investor rights are not already protected through other trade agreements. These treaties are designed to encourage the countries involved to adopt free-market policies that allow for more open investment by private companies.

BITs require that those who sign onto the agreement:

Treat US investments as favorably as domestic investments.

Have clear limits on foreign governments claiming investments (including repayment for any investments that are seized)

Don’t use performance requirements for operating an investment

Allow investors to work with the top managerial personnel of their choice when negotiating an investment.

Most importantly, BITs allow for investors of either party to advocate for their rights by submitting an investment dispute with the government of the other party to be settled by an international court.

NAFTA and US Trade

One of the most important US trade agreements in the last decades has been the North American Free Trade Agreement (NAFTA). NAFTA facilitated a large increase in goods trade between the US, Canada, and Mexico. In NAFTA’s first ten years, trade in goods increased from $293 billion in 1993 to $627 billion in 2003. By 2016, this value had increased to nearly $800 billion. Created in 1994, NAFTA was the world’s largest free trade agreement until it was replaced in March of 2020. Due to the Trump administration perceiving a disadvantage in America’s production of different industries relative to Mexico and Canada, namely in agriculture and automobile production, the United States-Mexico-Canada Agreement (USMCA) was established. Most concerning to the Trump Administration were trade deficits of $101 billion to Mexico and $27 billion to Canada as of 2019. The USMCA introduced several rule changes to automobile manufacturing, labor standards, the Canadian dairy and wine market, intellectual property, pharmaceuticals, and dispute resolution. This agreement went into effect on July 1, 2020. As of June 2021, the US trade deficit with Mexico has decreased to $52.9 billion and the trade deficit with Canada has decreased to $19.4 billion.

As discussed in the US-China Trade Deficit paper, the United States and China have a complicated economic relationship. While the two nations compete in many industries, they are also major consumers of each others’ goods and contribute on different points in a supply chain to produce many of the products in demand across the globe. At the same time, the trade deficit with China has caused growing concern in the United States, and caused many economists and policymakers to explore ways to better support US business in the face of competition with China.

I. Import Tariffs

An import tariff is a tax levied by one country on the goods and services imported from another country. Typically, governments impose these tariffs to protect domestic industries, gain additional revenue, and, in the case of the U.S.-China trade war, retaliate against unfair trading practices. Beginning in 2017, the United States imposed a litany of tariffs on Chinese imports, motivated by the expanding trade deficit. In theory, increasing the price of Chinese imports would drive up demand for domestically-produced goods and services, and, if the output increased to meet demands, would prompt domestic producers to hire additional workers. The import tariffs placed on Chinese goods and services would narrow the widening trade deficit and stimulate economic growth. However, many economists argue that the Trump administration’s import tariffs, when put into practice, achieved the complete opposite effect.

A recent report released by the U.S.-China Business Council (USBC) asserts that, contrary to the Trump administration’s goals, the tariffs actually “raised consumer prices on both imported products and domestic products.” The report also claims that by reducing consumer spending and stifling economic growth, these trade policies have cost the United States approximately 245,000 jobs. The Biden administration has since left these tariffs intact, a decision which Wall Street Journal columnist Henry Olsen deemed “welcome”. Olsen argued that to keep China from “[mounting] a serious challenge to U.S. global dominance,” the Trump administration’s burdensome tariffs must remain a necessary evil.

II. Import Quotas

Import quotas, a close cousin of import tariffs, achieve a similar objective through a different process. Historically, both have been utilized to reduce the volume of imports and encourage demand for domestically-produced goods. However, import tariffs are taxes on imported goods, whereas import quotas are limits on their quantity or monetary value. By many accounts, quotas are more effective in restricting trade since they aren’t affected by fluctuations in demand or exchange rates, but this isn’t a universally useful strategy. As Monica Sanders from the Houston Chronicle asserts, trading partners typically respond with similar trade restrictions, resulting in “less exporting opportunity for all producers and higher prices for all consumers.” For example, during the early 1980s, the United States imposed import quotas on Japanese automobiles to generate growth within the domestic auto industry. As economist Edward Hudgins remarks, by limiting the number of imported automobiles, domestic auto companies raised prices “without fear of losing business to less expensive competitors.”

III. Import Subsidies

Subsidies are government funds paid to domestic producers. Resembling other protectionist policies, subsidies protect against inexpensive foreign imports by decreasing production costs and, consequently, increasing production growth. This leads to increased demand for domestically-produced goods. While they do regulate costs and prevent the long-term decline of domestic industries, subsidies also lead to consumers bearing the brunt of the financial burden and can be complicated for infant industries. In order to collect funds for subsidizing domestic industries, governments must impose higher taxes. Since they develop without competition, subsidizing infant industries may eventually lead to those industries requiring permanent subsidies to stay afloat. Despite these potential risks, subsidies have remained a central component of U.S. trade policy over the last several decades. To encourage domestic energy production, the United States provides a number of subsidies to the fossil fuel industry. Totaling approximately $20 billion per year, these subsidies were initially intended to “lower the cost of fuel production and incentivize new domestic energy sources.” Due to comparatively cheaper renewable energy sources and negative environmental externalities, taxpayers have found it difficult to rationalize this government spending.

Since the establishment of formal diplomatic relations between the United States (US) and the People’s Republic of China (PRC) in 1979, there has been a rapid growth of bilateral trade. Trade in goods and services between the US and China increased from $15.4 billion in 1979 to $180 billion in 2000, growing at roughly 10% annually. This growth accelerated in 2000 when the US granted China permanent normal trade relations (PNTR), which paved the way for China’s accession to the World Trade Organization (WTO) in 2001. This served as a milestone in China’s “reform and opening” process and signified that the US and the global economic community recognized China as an equal partner. To join the WTO, China agreed to numerous conditions, including expanding market access for foreign firms to sell goods and services directly in Chinese domestic markets, lowering import tariffs, and opening the telecommunication and finance sectors to more foreign competition.

There is no doubt that WTO membership greatly benefitted the Chinese economy; expanded access to foreign markets increased net exports and economic growth as productivity increased due to greater competition. However, many in the US argue that China’s accession has hurt the US economy and workers, pointing to the ever-growing bilateral trade deficit, the loss of US manufacturing jobs and growing unemployment, and stagnating US economic growth as evidence that China has used unfair, if not illegal, trade practices to take advantage of the US. These trade practices allegedly include currency manipulation, government subsidies for land, capital, utilities and tax breaks, intellectual property (IP) theft, and lax environmental and worker health and safety standards. Furthermore, many criticize the WTO for its lax enforcement regarding China’s alleged illegal trade practices. While these trade practices have undoubtedly played a role in the bilateral trade deficit, a closer look reveals that it is only partly responsible for a stagnating US economy.

II.Background on Chinese Economic Growth

The People’s Republic of China was established in 1949 by the Chinese Communist Party (CCP). During this period, China struggled with unsuccessful socialist economic reforms and internal turmoil within the CCP. In 1978, Deng Xiaoping, a key political player under Chairman Mao, became paramount leader and began the ‘reform and opening’ process intended to jumpstart the Chinese economy and bring the country out of poverty. Deng echoed the sentiment behind these reforms later in 1992 when he stated:

“After the basic socialist system has been established, it is necessary to fundamentally change the economic structure that has hampered the development of the productive forces and to establish a vigorous socialist economic structure that will promote their development.”

Deng enacted a series of economic policies and reforms, particularly in industry and agriculture, that emphasized individual responsibility and greatly improved productivity. In 1986, China applied for membership in the General Agreement on Tariffs and Trade (GATT, the predecessor organization to the WTO). If granted entry, membership in GATT would greatly expand China’s export market as members would eliminate or reduce import tariffs on Chinese goods, and emphasize China as a destination for foreign direct investment (FDI).

Though Deng’s economic reforms successfully jumpstarted the Chinese economy, the country still struggled with extreme poverty and poor standard of living. China’s GDP per capita placed the country in the top half of low-income countries. In 1990, two-thirds of China’s population, or roughly 750 million people, were living below the International Poverty Line in extreme poverty, defined by the United Nations as living on less than 1.90 international dollars per day.

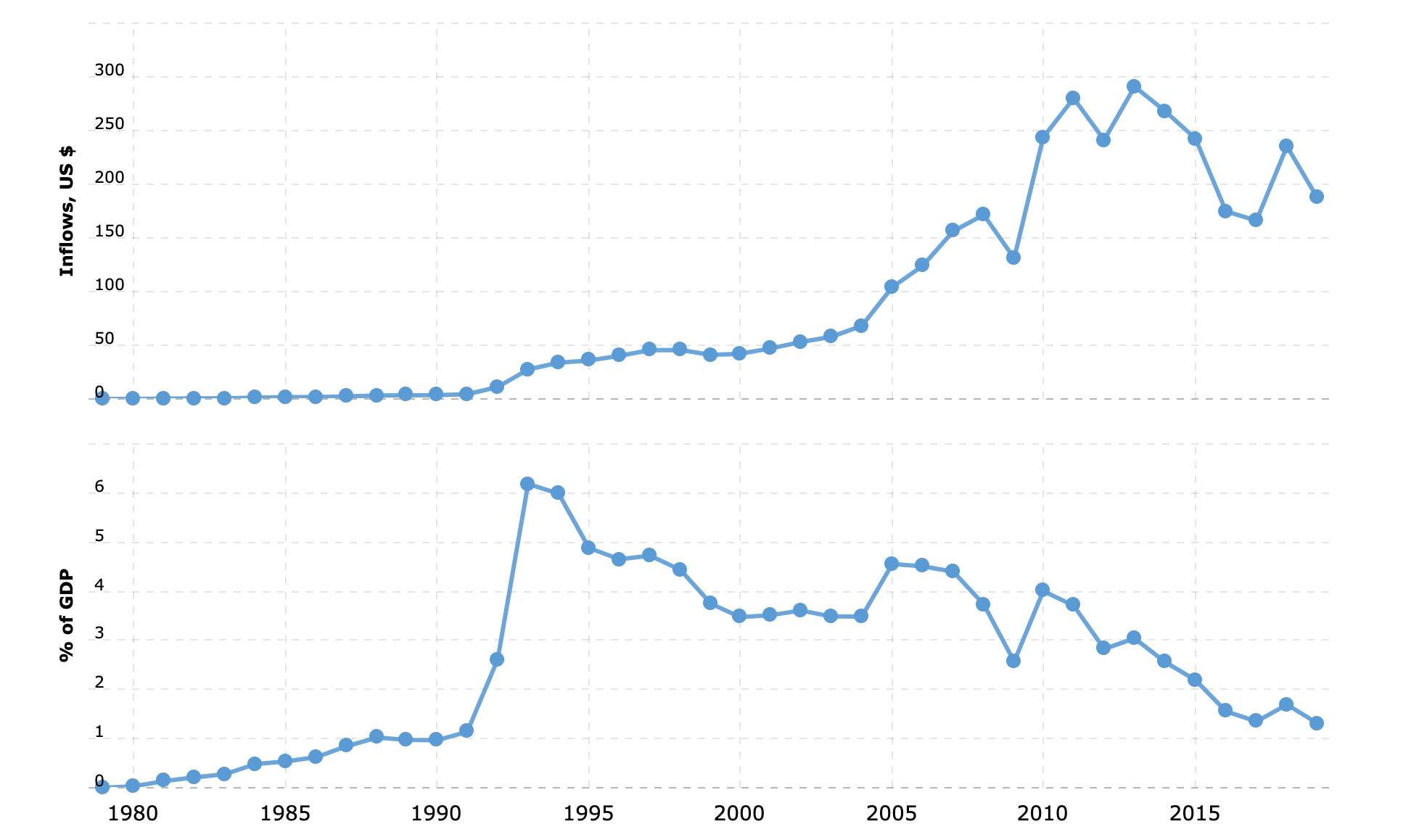

While foreign direct investment (FDI) increased by a factor of 13 between 1980-92 and 1986-88, the growth largely represents its originally low base. Additionally, though FDI inflows into China were large in the early 1990s, by the end of the decade the growth had stagnated. As shown in Figure 1, FDI inflow remained below 2% of gross domestic product (GDP) and below US$12 billion until 1992, mainly due to Chinese restrictions on FDI, government corruption, and inefficient state-owned enterprises (SOEs). FDI inflows did not begin to significantly increase until 2004, peaking at $290.9 in 2013.

The share of exports of goods and services in China’s gross domestic product (GDP) steadily increased in the 1980s and 1990s. However, total exports remained low as Chinese businesses had limited access to foreign markets and were subject to high import tariffs. Total exports did not begin to significantly increase until 2002, following WTO accession.

The Asian financial crisis in 1997 particularly affected Thailand, Malaysia, South Korea, and Indonesia. As the value of their currency dropped, there were rapid outflows of FDI and the stock market plunged. During this time, China held its exchange rate steady and provided a great source of stability for the region in addition to offering more than $4 billion in financial aid, a stark contrast to President Bill Clinton who described the Southeast Asian economies as temporarily experiencing a “few glitches in the road.” The crisis revealed the vulnerability of the Chinese economy, which was heavily dependent on cheap exports to fuel its rapid economic development. Since then, the Chinese government has emphasized the need to increase domestic consumption and reduce reliance on exports.

The US played a major role in China’s negotiations to join the WTO because the two countries had significant bilateral economic and trade interests, and because of US concerns surrounding how China’s exports would impact the international trade hierarchy. Negotiations stalled in June 1989 following the Tiananmen Square massacre and later in 1991 relating to unfair Chinese trade practices including import restrictions that built up net exports while Chinese companies evaded international rules on exports. Throughout the 1990s, China’s Most Favored Nation (MFN) status was increasingly political and tied to human rights concerns.

To join the WTO, China engaged in bilateral negotiations with each interested WTO member to establish market access concessions and commitments in the goods and services area, including tariffs on industrial and agricultural goods and Chinese commitments to open up its market to foreign services suppliers. China also undertook politically and economically risky reforms to uphold free market values of the WTO as a condition for membership. These included:

Increasing transparency of trade information and law to both foreign and domestic companies

Lowering import tariffs on agricultural and industrial products

Permitting foreign firms to sell directly in Chinese domestic markets

Opening the telecommunication and finance sectors to more foreign competition

Accession to the WTO triggered and accelerated internal domestic reform. WTO rules served China’s own goal of building a socialist market economy, set in 1992 by Deng, and aided in the transition from a decades-long planned economy to a market-oriented economy. Deng used membership requirements for accession to the WTO as a lever to achieve fundamental changes in SOEs and state-owned banks and overcome bureaucratic obstacles. Whereas Chinese import-exports used to be monopolized by a few dozen SOEs and ministries, after accession hundreds of thousands of Chinese enterprises became involved in import-export. This accelerated the volume of Chinese import-exports and expanded the variety of goods they offered. The central government lessened restrictions which previously constrained the private sector, encouraged private investment in industries that were traditionally dominated by SOEs, and reduced top-down control of Chinese enterprises. Productivity growth post-WTO accession also increased, driven by the entry and exit of firms increasingly allowed due to China’s decentralized reforms. SOEs faced greater accountability for their business decisions and faced the full forces of global competition for the first time, which placed pressure on domestic firms to lower their cost structure to survive. Firms that could not compete were forced to exit the market, increasing overall productivity.

China also reallocated labor and capital from farms to factories and from inefficient SOEs to more efficient private businesses. With China’s abundant labor supply and relatively scarce supply of arable land and natural resources, manufacturing was the primary beneficiary of reform-induced industrial restructuring. China’s reorientation toward manufacturing was further aided by substantial inflows of foreign direct investment (FDI). China accounts for 75% of all growth in manufacturing value added that has occurred in low- and middle-income economies since 1990.

Entrance into the WTO provided China with numerous benefits:

It was an important boost to China’s global leadership as it signaled the US and the global economy recognized China as an equal partner.

It strengthened US-China bilateral economic relations, which were strained over the issue of Taiwan and human rights violations.

Chinese exports could access new markets through Most Favorable Nation (MFN) status with all members of the WTO, which allows China to face the same trade barriers as competitors.

China experienced looser investment restrictions, which led to a growth in Chinese capital.

China no longer faced the uncertainty of being hit with high tariffs on its exports to the US. This encouraged Chinese firms to invest in paying the fixed costs associated with engaging in international trade and entering the export market. The US had applied low tariffs on Chinese imports since 1980, but every year Congress met to decide whether to revert to much higher tariff rates that had been assigned to some non-market economies, which averaged 24%.

Read More

Read more about other conditions for China to join the WTO here.

Read China’s White Paper from 2018 that lays out the government’s official position on the US-China trade relationship.

Read more about the role of state-owned enterprises in China’s economy here.

III.Impact of Increased Chinese Imports on the US Economy and Employment

A country’s total trade is measured by the sum of its imports (products it buys from other countries) and its exports (products it sells to other countries), both in goods and services. A trade deficit exists when a country’s net exports (calculated by subtracting imports from exports) is negative, meaning the country imports more goods and services than it exports. A trade surplus exists when the opposite occurs. The US has bilateral trade deficits with some trading partners and bilateral trade surpluses with others. Overall, the US had a trade deficit of $678.7 billion in 2020. Bilateral trade deficits typically occur because countries have certain comparative advantages. For example, the US has the comparative advantage in goods and services that require high degrees of human capital and China has the advantage in light manufacturing.

The US has had a trade imbalance with China since at least 1985 which remained below $85 billion. By 2000, however, the bilateral deficit reached $85 billion and for the first time exceeded the bilateral deficit with Japan. Between 1986 and 2019, the US trade deficit with China grew by 18.4 percent annually. Post-WTO accession, US exports increased as the US gained an export market, but not nearly as much as US imports from China increased. In 2007, US imports with China fell as consumers were hit hard by the recession and purchased fewer goods. US imports also decreased from 2018 to 2019 due to tariffs on Chinese products, though not as much as the decrease in exports.

With the recent 20th anniversary of the U.S. law implementing permanent normal trade relations with China, many politicians and political experts question President Bush’s decision to grant China PNTR status and allege that the Clinton administration and Congress rubberstamped both the law and China’s entry into the WTO. They argue that this fueled China’s rise and the “China Shock”—the period between 1999 and 2011 during which a sizable increase in Chinese imports supposedly produced the loss of approximately 2.4 million U.S. jobs.

Politicians who argue that trade with China has hurt the US economy also point to the decrease in US manufacturing output and in manufacturing employment. In 2000, 17.3 million US workers were employed in manufacturing, decreasing only 9% since the early 1980s. In mid-2007, right before the beginning of the Great Recession, manufacturing employment had already dropped to 13.9 million workers. During the Great Recession, manufacturing lost 20% of its output and 15% of its workforce. By 2010, a year after the Great Recession ended, employment had dropped to 11.5 million workers, a 33% decrease from 2000. Though the US aggregate contraction caused by the Recession undoubtedly contributed to the decrease in manufacturing employment, 60% of the decrease occurred before 2007. Additionally, employment levels have not recovered from the steep decline preceding the recession. Q2 2010 saw the first increase in US workers employed in manufacturing since 2006. By mid-2014, manufacturing employment had increased to 12.1 million workers, but nowhere near where it was in 2000.

Losses in US manufacturing employment are primarily due to the increase in Chinese manufacturing output, which intensified import competition for US firms who experienced a decrease in demand and a corresponding contraction in their workforce. Autor et al. (2013) and Pierce and Schott (2016) estimate the China Shock resulted in a loss of around 1.5 million manufacturing jobs between 1990 and 2007. Acemoglu et al (2014) found that had Chinese manufacturing imports to the US remained stagnant after 1999, there would have been 560,000 fewer manufacturing jobs lost through 2011. In a recent report, the Economic Policy Institute estimated that millions of jobs were lost because “imports displace goods that otherwise would have been made in the United States by domestic workers.”

An analysis by the Cato Institute reveals that new or continued U.S. restrictions on Chinese imports would not have saved the majority of U.S. manufacturing jobs lost during the period of the China Shock. Furthermore, Lincicome argues that China would have joined the WTO and become an economic powerhouse regardless of whether they had PNTR status from the U.S. Instead, he argues that a multitude of policy failures resulted in China’s ability to harm U.S. companies and workers. Some economists adopt an optimistic outlook and emphasize that the value added in manufacturing has been growing as fast as the overall US economy and the share of US GDP has remained stable, a feat experienced by only a few other high-income economies over the same period.

Economic linkages between sectors meant that the effects reverberated through the entire US economy. For example, China’s dominance in exporting apparel and furniture led to unemployment in other downstream industries that supplied US firms with the products necessary to make apparel or furniture. Additionally, much of the impact of increased trade exposure is felt in concentrated areas as suppliers and buyers are often found in the same regional market as to reduce transportation costs.

Many researcher argue that imports from China reallocated jobs from the manufacturing sector in lower human capital areas to the service sector in higher human capital areas. They find evidence of large manufacturing job losses, especially in areas of the US with initially low human capital such as the South and the Midwest, due to plant shrinkage and closures. These areas also experienced declining earnings per worker and little offsetting rise in service jobs. However, they find that areas with initially high human capital experienced limited manufacturing job losses. 50% of this effect is driven by industry switching, where surviving plants change their reported industry code from manufacturing to services (primarily research, management, and wholesale). Furthermore, they find no evidence that large, publicly listed U.S. manufacturing firms suffered from the rise in Chinese imports as their sales, investment, and market value were not affected. They hypothesize that these large firms took advantage of China’s comparative advantage in manufacturing production and exploited their cheap labor and lax environmental standards to offshore manufacturing employment. At the same time, large firms expanded employment in research, design, management, and wholesale activities in the U.S. Overall, Chinese trade weakened the market for labor in low human capital areas relative to high human capital areas and reallocated employment from manufacturing to services, and from US heartland to the coasts.

While manufacturing jobs did decrease as a result of Chinese manufacturing imports, overall US consumers have benefited from China’s accession to the WTO. The aggregate US manufacturing price index dropped by 7.6% between 2000 and 2006 due to China’s WTO entry. Two-thirds of this decrease in price index was due to China lowering their import tariffs in almost all categories of goods. By lowering tariffs on intermediate outputs, the cost of production for Chinese firms decreased, thus allowing them to charge lower prices on goods exported to the US and increase market shares in the US. Chinese exports to the US grew most rapidly in industries that experienced the largest drop in input tariffs. This also led other countries exporting to the US as well as US domestic firms to lower their prices as they received cheaper intermediate inputs from China. Inefficient firms that could not compete with Chinese firms exited the market. The other third was due to the increase in the number of firms and variety of goods exported to the US from China due to both lower input tariffs and China’s PNTR status. The number of Chinese firms exporting to the US more than tripled between 2000 and 2006.

While import competition from China undoubtedly contributed to US job loss, the growth of the information technology (IT) industry in the US and automation further exacerbated this shift in employment away from manufacturing. This shift especially hurt workers in regions of the US with low human capital as well as high-population states with large workforces. This is because automation displaces low-skilled workers while providing job opportunities for high-skill workers. Researchers from Ball State University found that nearly 88% of 5.65 million manufacturing job losses between 2000 and 2010 were due to automation and productivity increases, with trade accounting for just 13.4% of the losses. A study by the Carnegie Endowment for International Peace on manufacturing job losses in Ohio between 1969 and 2009 further found that trade accounts for no more than one-third of job losses. Rather, the majority of losses resulted from other factors, particularly automation and domestic competition with other states.

Furthermore, multifactor productivity (TFP), a measure of the change in an industry’s real output to changes in the combined inputs used in producing that output, was slowing down as output had already realized the gains from improved productivity. Between 1992 and 2004, manufacturing MFP grew by an average of 2% annually. However, between 2004 and 2016 manufacturing MFP declined by an average 0.3% annually. This slowdown of productivity growth coincided with the significant increase in import competition and with a reorganization of production and employment toward non-manufacturing services.

IV.Trade Deficit

The large and ever-increasing bilateral trade deficit between the U.S. and China has been an area of concern for politicians on both sides of the aisle, who emphasize the impact of WTO accession on the US trade deficit and see it as a weakening of the US economy. Many cite the China Shock as the reason for several negative macroeconomic factors including the U.S.’ slowing economic growth and stagnant wage growth. However, it would be incorrect and misleading to blame this on the large bilateral trade deficit between the U.S. and China. Rather, the bilateral deficit between two countries does not adequately reveal who is gaining or losing in a trade relationship and does not tell the whole story of the US-China trade relationship.

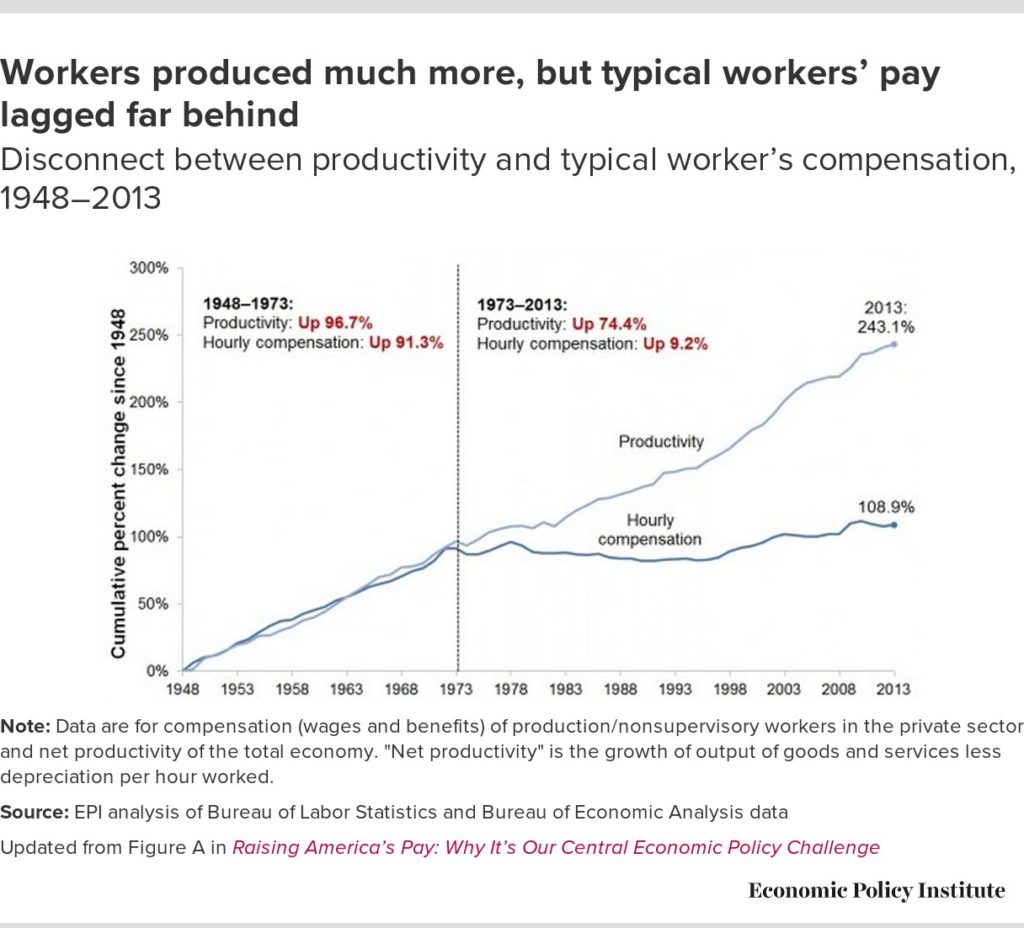

Productivity growth and real wages are closely linked. As productivity increases, workers can produce more output in the same or less amount of time, which enables employers to increase wages. However, as Figure 2 shows productivity in the US has been increasing but the typical worker’s compensation has not witnessed the same growth.

Previous economic research emphasizes two explanations for these features. First, globalization has flooded the market with cheap goods from China and eroded domestic manufacturing wages in the process. Second, technology has brought about automation which has destroyed manufacturing jobs.

However, as researchers from Kellogg Insight pointed out, US workers have struggled with wage stagnation for decades. Since the 1970s, growth in real wages, the value of the dollar paid to employees after being adjusted for inflation, has slowed compared to overall economic productivity. Furthermore, China did not begin to flood the market with cheap manufacturing exports until the mid-1990s, as seen in Figure 4. Lastly, job losses due to automation have primarily happened in the last 10 or 15 years. These three reasons suggest that import competition from China cannot be used as an explanation for stagnant wage growth and slowing economic growth.

Despite the causes of these two economic factors, US-China trade relations are a source of concern for many, especially with escalating trade tensions under the Trump and now Biden administration. The interdependence of the US and Chinese economies has served as an “effective brake” on escalating strategic distrust. Both President Biden and President Xi are working to reduce the reliance each nation has on the other.

Another source of stress stems from the US’ current accounts deficit, which is a measurement of a country’s trade where the value of the goods and services it imports exceeds the value of the goods and services which it exports. Because of this, the US typically borrows surplus savings from countries with current accounts surpluses and runs chronic current accounts deficits to attract more foreign capital. In 2020, China overtook Germany to become the world’s largest current account surplus. This was largely because the coronavirus crisis triggered higher demand for personal protective equipment and electronic devices, which boosted Chinese exports. China buys US treasury bonds using its current accounts surplus, and is the second largest US creditor, after Japan.

Many worry, however, that China will use its ownership of American debt as a bargaining chip to hold leverage over the US. However, the dollar is a widely-held and desirable asset in the global economy. While China has been the largest and second largest owner of US debt, the rest of the world (ROW) as well as individuals within the US still own the majority. For example, in August 2015, China reduced its holdings of US debt by roughly $180 billion, though this selloff did not significantly affect the US economy. Additionally, purchasing US debt enables China to manage the exchange rate of its currency, the renminbi. If China were to offload significant amounts of US debt, the exchange rate of the renminbi would rise and would make Chinese exports more expensive in foreign markets.

Continued US debt financing worries economists who are concerned that a sudden stop in capital flows to the US could spark a domestic crisis; though this would only happen if demand for US debt from all financial actors, foreign and domestic, suddenly stopped.

Despite the trade deficit, there are significant benefits to the trade relationship between the US and China. According to a study by Oxford Economics, trade with China supports roughly 2.6 million jobs in the US across a range of industries, including jobs that Chinese companies have created in the US. The continued growth of the Chinese middle class, projected to exceed the population of the US by 2026, also serves as an enormous opportunity for US companies to expand their customer base, which will help bolster employment and economic growth. Furthermore, China’s role in the global supply chain improves the competitiveness of US businesses and lowers US inflation.

Another factor that is often overlooked when tallying the balance of trade in the media is the contribution of US services exports to China. For example, trade data from the US Census Bureau only includes the trade of goods and not services. In 2019, the US exported $56.5 billion and imported $20.1 billion of services to China, a trade surplus of $36.4 billion. Chief US exports include capital products (22% of total exports), industrial supplies (22%), consumer goods (8%), and petroleum (7%).

That Washington and the media place such a high emphasis on the trade deficit with China but not with Japan and the European Union with whom the U.S. also has trade deficits suggests that the trade deficit is used as a scapegoat for other areas of concern that they have with China. These main areas include alleged human rights abuses (such as in Xinjiang or Hong Kong), theft of intellectual property, and more.

Read More

· Read this to learn more about trends in US real wages between 1979 and 2019.

V.U.S.-China Trade War

In the leadup to the 2016 presidential election, Donald Trump used inflammatory comments to call out China, including saying that China was “raping” the U.S. with unfair trade practices and that the country was responsible for the “greatest theft in the history of the world.” Strategically building off of the growing backlash against globalization, Trump pledged to “cut a better deal with China which would help American businesses and workers compete” and accused China of manipulating its currency to make its exports more globally competitive. Steve Bannon, senior White House advisor, claimed that globalists gutted the American working classes and created a middle class in Asia.

Once president, Trump renegotiated and revised trade agreements when US goals were not met. A key example of this is when he pulled out of the Transpacific Partnership (TPP), a multilateral trade agreement that would have created a single market for the US and the 11 countries that border the Pacific Ocean and would have maintained US trade dominance in Asia. Critics of the TPP argue that it would create wealth for multinational corporations rather than US workers.

Trump emphasized 1-on-1 bilateral negotiations with these Asian nations rather than joining the TPP, though he stressed that he would support future trade agreements if they were negotiated on a bilateral basis. This emphasis on bilateral negotiations demonstrates Trump’s belief that the global economy is a zero-sum conflict, where a gain for one party results in a corresponding loss for another party. Under this belief, multilateral negotiations result in allowing other countries to gain at the US’ expense. With bilateral agreements, the US would have greater leverage and be able to capture a greater share of the gains.

Trump’s 2017 Trade Policy Agenda stated that the overarching objective of the trade policy was to “expand trade in a way that is freer and fairer for all Americans.” To achieve this, the Trump Administration would increase economic growth, promote job creation in the U.S., promote reciprocity with the U.S.’ trading partners, strengthen the manufacturing base and the ability to defend the U.S., and expand agricultural and service industry exports. In a not-so-subtle dig at China, the Agenda states that the U.S. should not turn a “blind eye” to unfair trade practices that disadvantage American workers, farmers, ranchers, and businesses in global markets. Rather, Washington should act as “aggressively as needed to discourage” unfair trading practices and to encourage true market competition.

The Trump Administration executed this last statement with the ramping up of U.S.-China trade tensions in the first half of 2018 and the beginning of the trade war in July of 2018. A more complete timeline of the trade war can be found starting in Section 8. The US triggered the trade war starting in February 2018 with tariffs on solar panels meant to target Chinese firms and by initiating a WTO case against China. Trump increased these moves a month later targeting steel and aluminum imports. The next two years saw the imposition of tariffs, retaliatory tariffs, along with WTO cases alleging unfair trade practices from both the US and China.

VI.Effect of the Trade War on the US-China Trade Deficit

Tariffs are taxes paid on imported goods, previously used as a key source of government revenue but more recently used to shield certain industries from foreign competition.

Tariffs are generally paid through three sources.

Foreign companies exporting goods to the US.

Domestic companies importing goods from abroad or using imported inputs in their production processes.

American households as final consumers.

Despite Trump’s insistence that the $79 billion in tariffs were paid by foreign companies, multiple studies have found that this is not the case. One such study found that by December 2018, import tariffs were costing US consumers and the firms that import foreign goods an additional $3.2 billion per month in added tax costs and another $1.4 billion per month in deadweight welfare (efficiency) losses.

Despite President Trump’s claims that the trade deficit hindered US economic growth, real gross domestic product saw an overall decrease between 2017 and 2019, with growth rates increasing from 2.37% to 2.93% but then down to 2.16%. The trade balance is not the only factor contributing to US economic performance and growth, which includes factors like employment, productivity, age of population, and more.

VII.Conclusion

There are a multitude of factors causing the US-China trade deficit, not limited to the US current accounts deficit, Chinese currency manipulation, the shift in the US away from manufacturing jobs and towards service jobs, the growth of the information technology (IT) sector in the US and increased automation, and China’s comparative advantage in manufacturing that allows it to produce inexpensive goods. Furthermore, there are significant benefits to the US-China trade relationship, including lower aggregate prices for US consumers, and the promotion of at least 2.6 million jobs in the US. While increased import competition from China has resulted in the loss of several million manufacturing jobs, hitting the South and Midwest especially hard, overall trade with China has resulted in net job creation. Many view the US-China trade deficit as a sign of decaying US global leadership.

VIII.Timeline of US-China trade relations

1950-1972: US trade embargo with China

In late 1950, China intervened in the Korean War on the North Korean side. Anti-communist rhetoric and propaganda, fueled by the Cold War, contributed to the belief that China was an intrinsic threat to US national security, leading President Truman to retaliate by imposing a total trade embargo with China. At the time, bilateral trade was roughly $200 million annually. President Nixon ended the embargo in 1972 with the hopes that improved US-Sino relations would aid the US in the Cold War with the Soviet Union.

October 25, 1971: China joins UN

The PRC assumed the ROC’s place in the GA as well as its place as one of the five permanent members of the UN Security Council (UNSC).

February 1972: President Nixon makes historic trip to China to meet Chairman Mao

Nixon and Mao signed the Shanghai Communique, setting the stage for improved US-Sino relations by allowing China and the US to discuss difficult issues, particularly the China-Taiwan issue. For the rest of the decade, however, the two countries made slow progress in the normalization of their relations.

1973: First American business delegation visits China since the founding of the PRC

At the time, there was not much bilateral trade or investment because China did not have much to sell to the US and the Chinese did not want to buy from the Americans. The Chinese government was still wary of foreign influence and Chinese culture was not receptive to business with foreign companies, because they wanted to be self-reliant.

January 1, 1979: President Carter grants China full diplomatic recognition

Bilateral trade skyrocketed, creating a US trade surplus. At the time, the only investment model available for foreign companies was to establish a joint venture with a Chinese partner, which brought about conflicts with intellectual property (IP) theft.

1979: China and the US sign trade agreement

The trade agreement enabled Chinese products to receive temporary most favored nation (MFN) tariff status in the US. This made trading with China more attractive by lowering tariffs on goods imported to the US.

1980: Deng Xiaoping launches economic “reform and opening” in attempt to jumpstart China’s economy and improve standard of living

Deng expands access for foreign businesses in China and US, Japanese, and European investment flood China. China also joins the IMF and the World Bank.

Late 1980s and early 1990s: Surge of US investment into the PRC

China relaxed rules on foreign investment, including reforms which gave foreign companies permission to set up wholly foreign-owned enterprises in certain sectors, making it easier and more attractive to invest in China.

June 1989: Tiananmen Square protests

The crackdown on protesters in Beijing’s Tiananmen Square marked a turning point for US-China trade relations as investors question whether China is a healthy and stable market and as the US implemented economic and trade sanctions as punishment for Beijing’s human rights violation. US-China relations became a political argument, notably during the 1992 presidential election campaign when Democratic nominee Bill Clinton accused incumbent Republican George H. W. Bush of being “soft” on China, particularly in relation to human rights, as he resisted calls for punitive measures following the Tiananmen Square massacre.

1997: Asian financial crisis

October 10, 2000: US-China Relations Act of 2000

President Clinton granted permanent Normal Trade Relations (NTR) to China. This decision paved the way for China to ascend to the WTO. It reduced both tariff and nontariff barriers and fully opened the service sector to increased foreign ownership, especially in financial services, telecommunications, and distribution.

December 11, 2001: China enters the World Trade Organization (WTO)

After 15 years of negotiation, China finally gained accession to the WTO. It was a transformational moment in the global economy, marking the beginning of a new era of globalization. China’s trade with the world increased. The WTO is a global international organization that handles the rules of trade between nations to help producers of goods and services, exporters, and importers conduct business

2006: China surpassed Mexico as the US’ second-biggest trading partner, after Canada

2007: Chinese financial markets officially open to foreign investors under WTO rules

2008-2017: China signed free trade agreements with Association of Southeast Asian Nations (ASEAN) bloc and others

September 2008: China became the largest US foreign creditor

China surpassed Japan and owned around $600 billion in US debt. This marked a growing interdependence between the US and Chinese economies and concerns over US-China economic imbalances grew.

August 2010: China surpassed Japan to become the world’s second-largest economy

November 2011: US pivot toward Asia

Secretary of State, Hillary Clinton called for increased investment (diplomatic, economic, strategic, etc.) in the Asia-Pacific region as a move to counter China’s growing clout.

2015: China announced its Made in China 2025 plan

This was the first industrial policy to indicate that China was interested in and capable of capturing global market share in high-tech industries that had been traditionally dominated by Western companies.

2015: IMF added the Chinese yuan to its list of reserve currencies

February 3, 2016: Trans-Pacific Partnership is signed

Twelve countries (including the US), covering 40% of the world economy, signed the Trans-Pacific Partnership under President Obama. The TPP is advertised by President Obama as a “new type of trade deal that puts American workers first” and would help the US compete with China. The deal eliminated more than 18,000 taxes that various countries put on Made in America products. It also promoted a free and open internet, prevented unfair laws that restrict the free flow of data and information, and included the strongest labor standards and environmental commitments in history. The agreement included a 2-year ratification period in which at least 6 signatory countries must approve the final text for the deal in order for it to be implemented.

January 20, 2017: President Trump is sworn into office

He was known for having an “America first” economic platform and was skeptical of free trade norms. Trump felt that China was “ripping off” the US and taking advantage of free trade rules to the detriment of US firms operating in China.

May 2017: US Secretary of Commerce, Wilbur Ross, unveiled a 10-part agreement between Beijing and Washington to expand trade of products and services such as beef, poultry, and electronic payments. The agreement did not address more contentious trade issues including aluminum, car parts, and steel.

February 4, 2018: TPP was signed without the US

February 7, 2018: US implements new tariffs

The “global safeguard tariff” levied a 30% tariff on all solar panel imports (except those from Canada) and a 20% tariff on washing machine imports. Solar panel imports were worth $8.5 billion and washing machine imports were worth 1.8 billion

March 22, 2018: US filed WTO case against China

President Trump signed a memorandum filing a WTO case against China for their discriminatory licensing practices.

March 23, 2018: US put in place new steel tariffs

Following months of threats, President Trump announced major penalty tariffs of 25% on all steel imports (with the exception of Argentina, Australia, Brazil, and South Korea) and a 10% tariff on aluminum imports (with the exception of Argentina and Australia). President Trump claimed these imports “threaten national security” and target China’s alleged unfair trade practices. Steel imports were worth at least $60 billion.

April 2, 2018: China imposed retaliatory tariffs

China’s tariffs ranged from 15 to 25% on 128 US products worth $3 billion. This stoked growing fears of a trade war between the two biggest economies in the world.

July 6, 2018: US-China trade war officially began as US implements first China-specific tariff

The Trump administration imposed new tariffs on $34 billion of Chinese goods. More than 800 Chinese products in the industrial and transport sector faced a 25% import tax. China retaliated by imposing a 25% tariff on 545 goods originating from the US, worth $34 billion, including agricultural products, automobiles, and aquatic products.

August 3, 2018: China announced a second round of tariffs on US products

August 14, 2018: China filed a WTO claim against the US

The claim focused on US tariffs on solar panels and alleged that the US tariffs damaged China’s trade interests.

August 23, 2018: US and China implemented second round of tariffs and China filed a second WTO complaint against the US

China retaliated and imposed a 25% tariff on 333 goods, worth $16 billion.

September 24, 2018: US and China implemented third round of tariffs

October 4, 2018: Vice President Mike Pence delivered a critical speech against Beijing

Pence accused China of predatory economic practices, military aggression against the US, and of trying to undermine President Trump and harm his chances of winning re-election. Pence stated that the US will prioritize competition over cooperation by using tariffs to combat “economic aggression”

December 2, 2018: US and China agreed to a temporary truce

The truce aimed to de-escalate trade tensions, following a working dinner at the G20 Summit in Argentina. Both the US and China agreed to refrain from increasing tariffs or imposing new tariffs for 90 days as the two negotiated for a larger agreement.

December 14, 2018: China temporarily lowered tariffs on US automobiles for three months.

US auto imports are subjected to China’s standard 15% tariff rate on foreign autos. The suspension of additional tariffs is extended on March 31, 2019.

April 1, 2019: China banned all strains of fentanyl

Chinese fentanyl production and distribution had been a source of tension in bilateral relations because of the opioid crisis in the US.

April 10, 2019: US and China agreed to establish trade deal enforcement officers to monitor the enforcement of the trade deal, which has not yet been finalized

May 10, 2019: Trade war intensified

The US increased tariffs on $200 billion worth of Chinese goods from 10% to 25%. President Trump stated that he believes the high costs imposed by the tariffs will force China to make a deal favorable to the US.

May 13, 2019: China retaliated and announced it will increase tariffs on $60 billion worth of US goods starting June 1

May 16, 2019: US Department of Commerce announced the addition of Huawei Technologies Co. Ltd and its affiliates on its “entity list,” which effectively banned US companies from selling to the Chinese telecommunications company without US government approval.

June 2, 2019: China issued a white paper on US-China economic relations found here.

The paper denounced US unilateral and protectionist measures, criticized its backtracking on Sino-US trade talks, and demonstrated China’s stance on trade consultations and the pursuit of reasonable solutions.

June 21, 2019: US Department of Commerce added 5 more Chinese companies to its “entity list”

Sugon, the Wuxi Jiangnan Institute of Computing Technology, Higon, Chengdu Haiguang Integrated Circuit, and Chengdu Haiguang Microelectronics Technology were added to the list.

August 6, 2019: US Treasury labeled China as a currency manipulator

The yuan sank to 7 against the US dollar in apparent retaliation to the new punitive tariffs threatened to apply on the remainder of Chinese imports. China denied the accusations. The US later dropped this designation days before signing the phase one trade deal.

August 23, 2019: China announced $75 billion in tariffs on US goods.

September 1, 2019: US began implementing tariffs on more than $125 billion worth of Chinese imports.

September 2, 2019: China lodged a WTO tariff case against the US

According to WTO rules, the US has 60 days to try to settle the latest dispute.

October 11, 2019: President Trump announced that the US and China have reached a “Phase 1” agreement and that the US will delay a tariff increase.

November 1, 2019: WTO stated that China can impose compensatory sanctions on US imports worth $3.6 billion for the US failure to abide by anti-dumping rules on Chinese products.

January 15, 2020: US and China signed the ‘Phase 1’ trade deal, easing 18-month trade tensions

The trade deal relaxed some US tariffs on Chinese imports and committed China to buying an additional $200 billion worth of American goods (including agricultural products and cars) over 2 years, though the majority of tariffs remain in place

January 20, 2021: President Biden is sworn into office and planned to remain tough on China

Cabinet members signalled that Biden plans to take a multilateral approach by enlisting the support of Western allies to maximize Washington’s leverage on Beijing.

The business cycle is the fluctuation of total economic activity over time. Recessions occur when total economic output, measured by Gross Domestic Product (GDP), grows at a negative rate for at least two quarters in a row. These downturns occur after the economy reaches its peak. Once GDP growth becomes positive again, the economy rebounds from a trough and begins expansion. The National Bureau of Economic Research (NBER) Dating Committee is the most accepted resource for dating recessions.

Unemployment moves through a cycle within expansions as well. After the economy adds jobs consistently during the beginning stages of an expansion, it approaches full employment. Once full employment is reached, real wages tend to increase. Real wage growth typically ends in two scenarios: when inflation reduces workers’ purchasing power, or when the economy hits its peak, starting the business cycle once more.

We can visualize how unemployment changes with GDP growth over time in Figures 1 & 2.

Dips in GDP growth correspond with higher unemployment, and unemployment tends to be at its lowest at the end of an expansion period. Macroeconomists term this relationship Okun’s Law after the American economist Arthur Okun who first observed this relationship. This relationship has held up empirically since it was first proposed in 1962. Figure 3 demonstrates this relationship’s consistency.

The nature of the business cycle has not remained constant in the long term. When the United States economy was consistently growing at upwards of 3% annually, the economy went through the business cycle in shorter, more volatile intervals. However, after a recession in the early 1980s, the business cycle became less acute and more predictable, with expansions lasting longer than in previous economic eras. This dynamic is termed the Great Moderation, as economic growth also moderated with the business cycle. In fact, the two longest expansions in United States history have occurred within the last 20 years, even though year-over-year growth decreased relative to pre 1980s levels. The lengthening of expansions becomes clear when we visualize each expansion in Figure 3.

How have business cycles affected me and my community in the past?

If we are currently at the beginning of an expansion, what type of macroeconomic trends should I expect?

Which is preferable: longer expansions with smaller year-to-year growth, or shorter expansions with higher growth, more similar to pre-Great Moderation business cycles?

How does the business cycle affect the way I vote?

The American Rescue Plan Act of 2021, or American Rescue Plan, is a COVID-19 stimulus bill consisting of a package of roughly $1 trillion towards economic recovery and assistance in response to the Coronavirus Pandemic. The American Rescue Plan, or ARP, was signed into law by President Biden on March 11, 2021 as an extension of the previous stimulus package. The passing of the ARP comes a year after the Coronavirus Aid, Relief, and Economic Security Act, or the CARES Act, which was signed into law by President Trump on March 27, 2020.

Components of the ARP

The ARP contains many extensions of provided benefits under the CARES Act. One of the prominent extensions included in the ARP is the Pandemic Unemployment Assistance, or the PUA, which is an unemployment insurance program that covers unemployment benefits for qualifying citizens. Under the CARES Act, the PUA was scheduled to terminate in December of 2020 after providing 39 weeks of benefits. This timeline has been extended to 79 weeks under the ARP, providing benefits through September 6, 2021. However, the ARP only gives states the option to extend unemployment benefits, since the power to give out unemployment benefits rests with individual states.

The ARP also provides pandemic relief for state and local governments through “$219.8 billion, available through December 31, 2024, for states, territories, and tribal governments to mitigate the financial consequences of COVID-19.” This funding is directed to be used as pandemic relief, such as assistance for households, small businesses, nonprofits, or commercial industries; increasing employee wages or providing grants to employers; aiding to resolve the reduction in state revenue, territories or tribal governments; and investing in infrastructure.

The bill also provides relief via tax cut: for people who claim the extended unemployment benefits, up to $10,200 will be waived from their federal taxes. This component of the law will have the largest effect on the deficit according to the Congressional Budget Office.

Critiques of the ARP

Many argued the ARP was unnecessary considering unemployment rates showed a decreasing trend months before the ARP was passed (seen in Figure 1 and Figure 2). National and state unemployment rates were increased by the consequences of COVID-19. However, these trends shifted after the first stimulus packages from the CARES Act came into effect, causing a steady decrease in national and state unemployment rates through late 2020 and into 2021. The ARP was passed in March of 2021 while unemployment rates were decreasing throughout the United States. This led some economists and politicians to consider the plan excessive or unnecessary, as the ARP includes not only stimulus covering the repercussions of the health crisis, but also a multitude of unemployment programs.

The above graph displays the United States’ national unemployment rate between 2005 and 2021. After hitting a peak of 14.8% in April of 2020, the unemployment rate began a steady decline, reaching 5.8% in May of 2021.

Disputes over the unemployment provisions of the American Rescue Plan remain contentious and are largely fueled by a fundamental disagreement over the role of government in economic policy. One side advocates for laissez-faire capitalism—a system in which the government stays out of the economy and allows individuals to independently make economic decisions. The other is in favor of a more Keynesian approach. Keynesian economics theorizes that increased government spending and lower taxes are necessary during economic downturns in order to stimulate the economy. Those who support Laissez-faire economics believe that government intervention in free markets creates market distortions in the long run, in this case potentially discouraging those receiving benefits from actively seeking new employment. There are further concerns that these temporary provisions may remain in place even after the economy recovers, resulting in a soaring deficit. On the other hand, believers in Keynesian economics argue that the government has a responsibility to provide bailouts and other forms of support to citizens during recessions. Proponents of this view point out that shutdowns in the interest of public health caused unemployment to soar and argue that the unemployment compensation will bolster the economy.

The debate over this provision boils down to a debate over liberty versus equity, with advocates for liberty arguing in favor of lower taxes and minimal social safety nets, while advocates for equity argue that greater public welfare is more important than lower taxes. Equity proponents point to studies that estimate the expansion of the child tax credit could reduce child poverty in the US by 45%, lifting millions of children out of poverty. Conversely, liberty proponents say that money belongs to those who earn it, that private individuals use capital more efficiently than the government, and that high taxes discourage investment.

The ARP also designates nearly $350 billion for states’ budgets, which cannot run deficits in the same manner as the national government. $220 billion of those funds are for states to balance their budgets, which have suffered as a result of the COVID-19 recession, according to the Biden administration. The rest of the funds are specifically designated for states in dealing with the COVID-19 pandemic and its economic focus on reopening in-person primary education. The two categories of education relief are funds to address learning loss due to online schooling and virus mitigation efforts in school, particularly improving ventilation.